All Articles

Britain Is Literally Paying a Per-Wife Bonus With Taxpayer Money — And No, This Isn't Satire

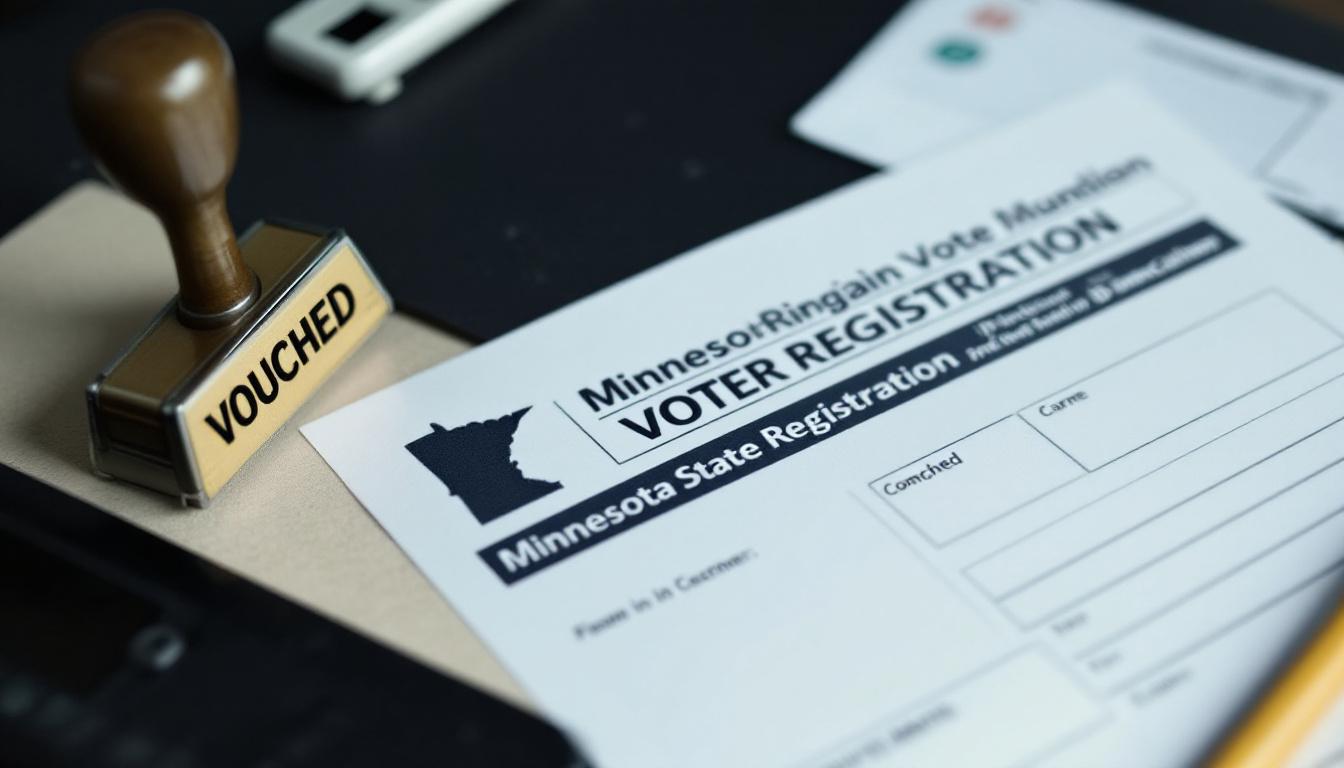

2026-05-08Minnesota's Running Elections on the Pinky-Swear System — And They Won't Even Track Whether It's Being Abused

2026-05-08Britain Is Literally Paying a Per-Wife Bonus With Taxpayer Money — And No, This Isn't Satire

2026-05-08Minnesota's Running Elections on the Pinky-Swear System — And They Won't Even Track Whether It's Being Abused

2026-05-08Britain Is Literally Paying a Per-Wife Bonus With Taxpayer Money — And No, This Isn't Satire

2026-05-08

Left-Wing Activist Tried to Firebomb the Texas GOP Headquarters — And Left a Handwritten Confession Note Because Apparently Arsonists Are Getting Dumber

2026-05-08

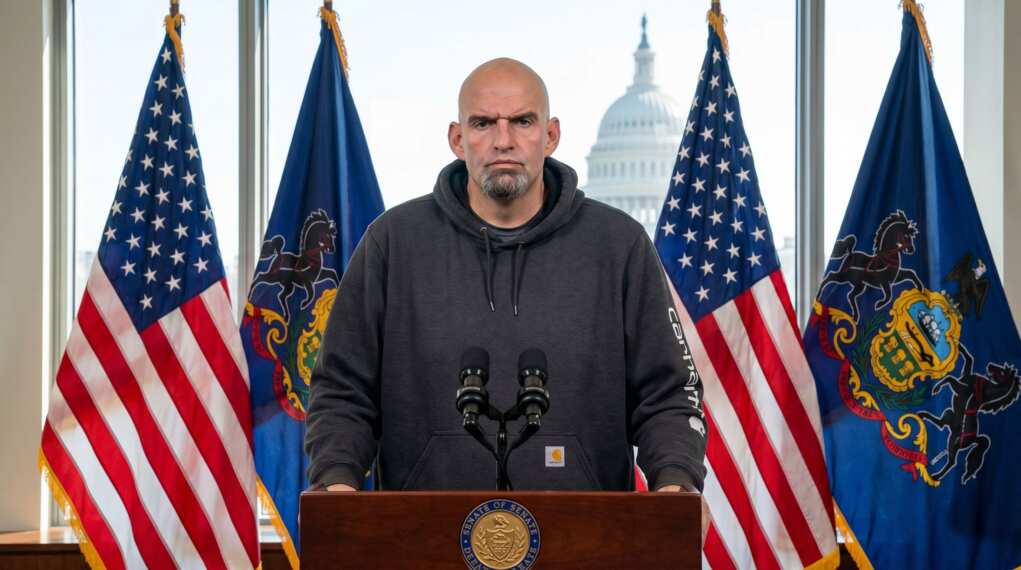

Fetterman Just Shut Down Donna Brazile on Live TV Over Iran — And Liberals Don't Know Whether to Cry or Pretend It Didn't Happen

2026-05-08

A Sitting American Mayor Was Literally a Chinese Spy — And the Media Couldn't Be Bothered to Mention It

2026-05-08

He Was Released From a Psych Ward at 5 PM — By 10 PM a 76-Year-Old Retired Teacher Was Dead

2026-05-08

ICE Just Arrested a Child Sex Offender Who Was Walking Free in Tennessee — Remind Me Why We're the Bad Guys?

2026-05-08

He Got Censored for Telling the Truth About COVID Vaccines — The Government Paid Up, and Now Pfizer's CEO Is Next

2026-05-08

Israel Is Suing the New York Times for Making Up a Rape Story — And the Paper of Record Is About to Become the Paper of Record Settlements

2026-05-08

The Government Just Wrote a $150,000 Check to a Reporter They Censored — Every 'Conspiracy Theorist' Who Called It Was Right

2026-05-08

The U.S. Military Just Destroyed 90% of Iran's War Machine in 40 Days — And the Media Forgot to Mention It

2026-05-08

Newsom's Chief of Staff Just Pleaded Guilty to Stealing Campaign Cash

2026-05-08

American Secret Service Agents Stared Down Chinese Security for 30 Minutes — And Didn't Blink Once

2026-05-08

Tennessee Democrats Just Lost Their 20-Year Grip on Memphis — And All It Took Was Drawing an Honest Map

2026-05-08

SCOTUS Just Shredded Democrats' Crayon-Drawn Virginia Map — And Spanberger Is Already Making Excuses

2026-05-08

They're Literally Angry About Prayer in a Building Where People Have Prayed for 226 Years

2026-05-08

A Mexican Senator Was Literally on the Cartel Payroll — And He Got Nabbed the Second He Set Foot in San Diego

2026-05-08

Psaki Lied From the White House Podium for Two Years — Now She's Lying From MSNBC and Eric Trump Is Sending Lawyers

2026-05-08

130 Lawsuits. 32 States. The RNC Finally Stopped Complaining and Started Suing.

2026-05-08

Trump Created a $1.776 Billion Fund to Fight the Deep State — And the Dollar Amount Is the Best Part

2026-05-08

Teachers Buy Their Own Crayons While Union Boss Randi Weingarten Blew $1.4 Million of Their Dues on Her Vanity Book

2026-05-08

Sean Duffy Buries Kirsten Gillibrand With Her Own $7 Million Trial Lawyer Tab in Explosive Senate Hearing

2026-05-08

Trump's Border Crackdown Is Saving Taxpayers a Fortune — and the Media Is Dead Silent

2026-05-08

They Knew for 23 Years: UK Rape Gang Finally Gets Nearly 300 Years — After Authorities Kept It Quiet

2026-05-08

The DOJ Wants to Know What Drugs Were Prescribed to Children. Someone Is Spending a Lot of Money to Stop Them.

2026-05-08

Trump Admin Funnels All Ebola-Nation Flights Through One Airport to Protect Americans

2026-05-08

Minnesota Fraudster So Terrified of Trump's DOJ He Literally Jumps Off a Building

2026-05-08

Woman Beheads Jesus Statue Outside Long Island Church — Cops Still Deciding If It's a 'Hate Crime'

2026-05-08

Trump Admin Moves Lawyers Like Chess Pieces to Speed Up Kicking Fraudulent Citizens Out of the Country

2026-05-08

Trump's Iran Deal Could Drop Today — And Your Portfolio Is About to Notice

2026-05-08

CBS Host Tries to Get Medal of Honor Heroes to Trash America on Memorial Day — Gets a Patriotism Lesson Instead

2026-05-08

Kansas City Tells Christians: We Don't Care What the Supreme Court Says, You'll Counsel Who We Tell You To

2026-05-08

YMCA in Liberal Town Forced to Reverse Transgender Locker Room Policy After 17-Year-Old Girl Sees Exactly What You Think She Saw

2026-05-08

Illegal Alien Goes on 28-Hour Shooting Rampage Across Austin — Fires at Homes, Cars, and Firefighters Trying to Save Lives

2026-05-08

The 'Hunger Strike' That Wasn't: DHS Pulls the Receipts on NJ Democrats' Detention Center Hoax

2026-05-08

Fox News Reporter Gets Called a 'Nazi' on Live TV — Her Response Is Pure Gold

2026-05-08

NC Court Confirms Non-Residents Voted in Federal Elections — But Sure, Election Integrity Is a 'Conspiracy Theory'

2026-05-08

They Fired 1,500 Healthcare Workers Over the COVID Jab — Now the Feds Want the Supreme Court to Forget It Ever Happened

2026-05-08

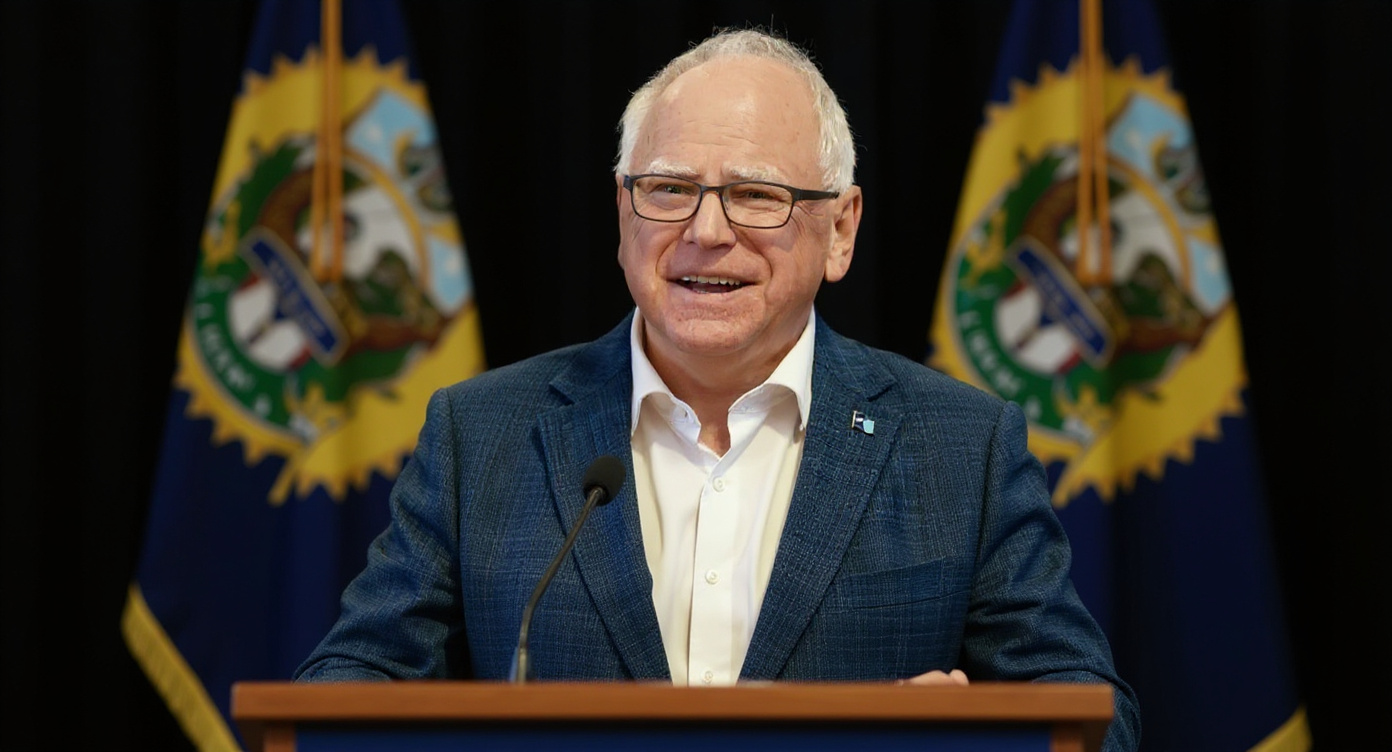

Governor Walz Calls Emergency Session — Not for a Disaster, But to Pardon an Armed Robber Before ICE Shows Up

2026-05-08

Judge Slams the Door on Democrats Trying to Block Trump's Mail-In Voting Order

2026-05-08

America Is Sitting on a Mineral Goldmine — And We Finally Stopped Pretending It Doesn't Exist

2026-05-08

Family Federally Indicted for Beating Up a Reporter Now Playing Victim With Restraining Orders Against HER

2026-05-08

Karen Bass Put a Convicted Killer on the City Payroll and Called Him a 'Peace Ambassador'

2026-05-08

MSNBC's Symone Sanders Calls ICE Agents 'Monsters' — Because Enforcing the Law Is Scary Now

2026-05-08

Blue-State Sheriffs Tell Their Own Democrat Governors to Pound Sand — And It's Beautiful

2026-05-08

Media Finally Forced to Cover Democrat's Sex Scandal — Democrats Respond by Rallying Behind Him Anyway

2026-05-08

CBS Legend Calls It 'Murder' When Someone Brings Actual Journalism to 60 Minutes

2026-05-08

NYC's New Communist Mayor Wants to Seize Your Apartment Building — And He's Got a 111-Page Plan to Do It

2026-05-08

NIH Scientists Caught Smuggling 113 Vials of Monkeypox Through Detroit — And They Lied About It

2026-05-08

Squad-Backed Democrat With Al-Qaeda-Linked Ties Just Won His Primary — And the Media Yawned

2026-05-08

Code Pink 'Peace' Activist Smacks Rep. Anna Paulina Luna — Because Nothing Says Anti-War Like Assaulting a Congresswoman

2026-05-08

Trump Calls Netanyahu 'Crazy' to His Face — And That's How Real Diplomacy Works

2026-05-08

Corporate America Just Ghosted Pride Month

2026-05-08

Democrats Spent a Century Owning South Texas — Now They Can't Even Read the Room

2026-05-08

Sen. Chris Murphy Caught Bankrolling Anti-ICE Protest Machine With $100K PAC Check

2026-05-08

Nearly Half of Minneapolis Immigrants Caught Committing Fraud

2026-05-08

CBS Anchor Scott Pelley Claims He's 'Been in Combat' — Then Cries About It on Camera

2026-05-08

UK Deputy PM Says the Quiet Part Out Loud — Equality Doesn't Mean 'Equal' Anymore

2026-05-08

Bill Gates Has to Explain His Epstein Hangouts Under Oath — Pass the Popcorn

2026-05-08

Left-Wing Nonprofit Secretly Embedded Lawyers in State Offices to Prosecute Trump Supporters — The Receipts Are Out

2026-05-08

Vance Just Referred Tim Walz to the DOJ for Criminal Fraud — Remember When He Said 'Trust Me'?

2026-05-08

Stanford Hands Drag Troupe $50,000 — Veterans Get a Measly $10,000 Because Priorities

2026-05-08

Migrant Gouges Out Man's Eye in Belfast — UK Government Blames Twitter

2026-05-08

California Hoovers Up 80% of Every Federal Dollar Spent on Illegal Immigrant Families

2026-05-08

Someone Carved a Death Threat Against Trump Into the National Mall — Media Yawns

2026-05-08

81 Percent of Claims in LA's $4 Billion Sex Abuse Settlement May Be Fake — The Grift of the Century

2026-05-08

Florida Sheriff Calls Child Predators 'Pieces of Sh*t' on Live TV — And America Cheers

2026-05-08

Biden Judge Now Decides What Signs Hang in National Parks — Orders Trump Admin to Restore Climate and Slavery Displays

2026-05-08

Jim Acosta Compares Removing Trump's Name from the Kennedy Center to the Fall of the Berlin Wall — And He Wasn't Joking

2026-05-08

Giants Pitcher Landen Roupp Stands Tall for His Faith on Pride Night — In San Francisco, No Less

2026-05-08

JD Vance Is Walking Into Enemy Territory — And Making Them Regret It

2026-05-08

When You've Lost Fareed Zakaria, You've Lost Everything — CNN Host Torches California's Democrat Disaster

2026-05-08

Senate Smacks Down Democrats' Desperate Attempt to Handcuff Trump on Iran

2026-05-08

Haitian National Stole $58 Million From a Program Meant for Sick Americans — Now He's Going to Prison and Getting Deported

2026-05-08

Trump Walks Into the G7 and Tells Every World Leader 'I'm the Boss' — Not One of Them Argued

2026-05-08

Hollywood Can't Sell Tickets Anymore So Adam Schiff Wants YOU to Bail Them Out

2026-05-08

Thirteen Months, Zero Releases: Trump Just Made 'Impossible' Border Security Look Easy

2026-05-08

The Obamas Built a Monument to Themselves — and Stiffed the Workers Who Actually Built It

2026-05-08

Gallego and Swalwell: The Buddy-Cop Donor Cash Blowout Nobody Asked For

2026-05-08

Keir Starmer's Socialist Experiment Crashes and Burns in Record Time

2026-05-08

Zuckerberg Privately Warned His Execs Against the Vaccine While His Platform Censored You for Saying the Same Thing

2026-05-08

China Just Sanctioned the Companies That Build Our Weapons — And the Ones That Mine the Minerals to Make Them

2026-05-08

Bill Pulte Shows Up to Work on Friday, Starts Handing Out Pink Slips by Monday

2026-05-08

Whoopi Goldberg Wants Trump Sued Over a Reflecting Pool. An Illegal Alien Just Plotted to Attack the White House.

2026-05-08

JPMorgan's DEI Executive Fired After Viral Video Shows Her Dumping Trash in the Street to Steal a Knicks Souvenir

2026-05-08

New York Democrats Just Got Eaten by Their Own Radicals — and It Wasn't Even Close

2026-05-08

You Need ID to Buy Sudafed But Not to Vote — Thanks to an Obama Judge

2026-05-08

Fetterman Tells Larry David to 'Get Over Yourself' After Curb Creator Calls White House UFC Night a 'Travesty'

2026-05-08

Feminist Fashion Critics Attack Usha Vance's $8.75 Old Navy Dress — The 'Women Supporting Women' Crowd Has Conditions

2026-05-08

CNN Drops the Mask: Van Jones Celebrates 'The Revolution Is Being Televised' as Socialists Sweep New York

2026-05-08

New York Times Discovers Air Conditioning Is a Far-Right Plot to Not Die of Heatstroke

2026-05-08

Buttigieg's Swatting Story Starts Falling Apart Before the Media Finishes Crying

2026-05-08

DHS Secretary Mullin Hits 100 Days and the Deportation Numbers Are Embarrassing — For the Last Administration

2026-05-08

Iran Blinked: After Getting Hit, Tehran Signs a Ceasefire and Asks to Talk

2026-05-08

DOJ Comes Knocking for Arizona Democrat Who Blew Campaign Cash on Super Bowl Tickets and Disney World

2026-05-08

CNN Ran a Gas Price Scoreboard When Prices Were High — Scott Jennings Noticed They Unplugged It

2026-05-08

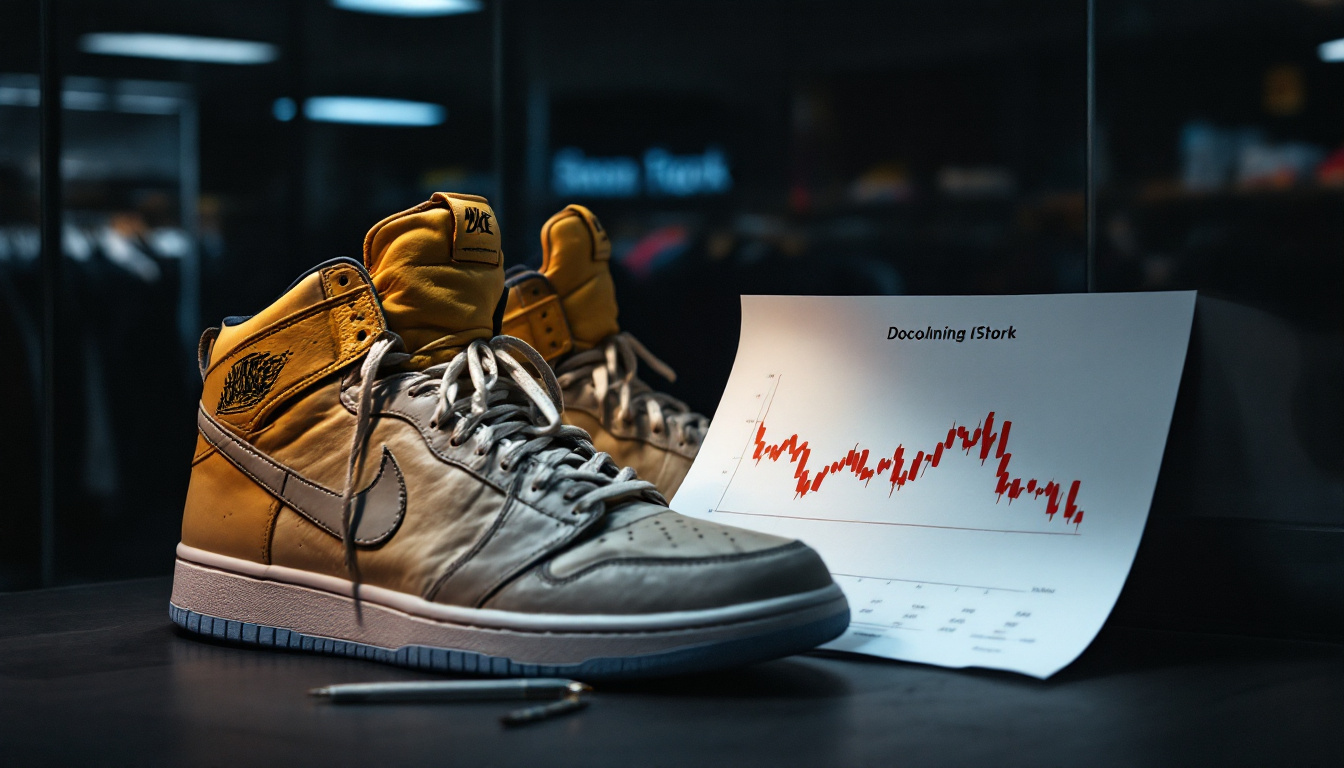

Nike Traded Michael Jordan For Colin Kaepernick And The Stock Chart Tells You How That Went

2026-05-08

North Carolina Just Killed Sanctuary Policies Statewide — And The Way They Did It Is Even Better

2026-05-08

A Warning to Washington: Tucker Carlson to Build a Third Party After Leaving the GOP

2026-05-08

Trans Democrat Admits Trump's 'They/Them' Ad Worked — Blames Own Party for Choking

2026-05-08

62% of Democrats Would Vote for a Socialist — And They Want You to Know It

2026-05-08

Buffalo Canceled America's 250th Birthday Fireworks — Then Raised the Somali Flag Over City Hall

2026-05-08

WaPo Spends July 4th Red-Penning the Declaration of Independence

2026-05-08

The View Couldn't Fake Patriotism for One Episode on America's 250th Birthday

2026-05-08

Paul Pelosi Hits Another Car and Drives Off — But Don't Worry, He Wasn't Drunk This Time

2026-05-08

Speaker Johnson Says Mamdani Was Just the Opening Act — The DSA Has a Whole Roster Coming

2026-05-08

Feds Finally Pull the Plug on Taxpayer-Funded Degrees That Pay Less Than a High School Diploma

2026-05-08

Warren Called Him 'My Kind of Man' — Now She Wants Him Gone After Rape Accusation

2026-05-08

Judge Reinstates Voter Roll System That Biden Judge Blocked — Turns Out the Constitution Still Works

2026-05-08

Toyota Moving Tacoma Production From Mexico to Texas — $3.6 Billion and 2,000 Jobs Say Tariffs Work

2026-05-08

The Networks Spent 27 Hours on Epstein in One Year — And Still Couldn't Find a Single Democrat

2026-05-08

California Won't Prosecute Shoplifters but Wants to Fine Pro-Life Groups $20 Million for Helping Pregnant Women

2026-05-08

Vance Drops Subpoenas on Silicon Valley's Favorite Cheap-Labor Scam

2026-05-08

Sixty Countries Sit Down to Discuss the Terrorism Your Professor Said Didn't Exist

2026-05-08

Railway Conductor Gets Fired for Saying 'Happy Independence Day' — Americans Respond With $15,000

2026-05-08

Iran Closed a Shipping Lane. The US Hit 140 Targets. Questions?

2026-05-08

Hunter Biden Is Producing His Own Propaganda — And the Media Is Distributing It for Free

2026-05-08

Israeli Ambassador Dismantles Ro Khanna's West Bank 'Detention' Story on Live Television

2026-05-08

A Leftist Mob Chased a Man Out of a Concert for Wearing the Wrong Hat — And Then Bragged About It Online

2026-05-08

The Feds Had to Do Karen Bass’s Homework — Shut Down LA’s Most Infamous Drug Market While She Pretended It Didn’t Exist

2026-05-08

Republicans Outraise Democrats by More Than $10 Million Six Months Before Midterms — And the DNC Is $18 Million in Debt

2026-05-08

They Leaked WAR PLANS While US Navy Ships Were Literally Under Fire — And Nobody’s in Handcuffs

2026-05-08

Women Prisoners Sue Washington State for Locking Them in Cells With a Six-Foot-Four Male Sex Offender Who ‘Identifies’ as Female

2026-05-07

Biden’s DHS Released a Nicaraguan Illegal Into America — Now He’s Charged With Sexually Assaulting Elderly Nursing Home Patients

2026-05-07

Turns Out Locking Up Criminals Reduces Crime — And It Only Took Democrats Fifty Years to Figure It Out

2026-05-06

The New York Times — America’s Diversity Police — Just Got Sued for Discriminating Against a White Guy

2026-05-06

The Arsonist Who Burned LA Worshipped a Left-Wing Assassin — And ABC and CBS Won’t Tell You

2026-05-05

They’re Awarding Pulitzer Prizes for Trump Derangement Syndrome Now — And the ‘Journalists’ Are Celebrating Like They Actually Did Something

2026-05-05

A 400-Acre Islamic City Is Being Built Outside Dallas — And the Guy Running for AG Just Promised to Bulldoze the Permits

2026-05-04

Every Blue City in America Is Going Broke — And They All Have One Thing in Common

2026-05-04

Did Hell Freeze Over? PolitiFact Accidentally Told the Truth

2026-05-04

Elizabeth Warren Celebrated Killing Spirit Airlines — Now Thousands of Stranded Passengers Would Like a Word

2026-05-04

Biden Drained the Oil Reserve for Votes. Trump Just Used It the Right Way.

2026-05-01

Seven Democrat House Seats Just Landed on the Chopping Block — And the Left Is Having a Full Meltdown

2026-05-01

They’re Not Just Indicting Comey — They’re Taking His Book Money

2026-05-01

Teacher Unions Blew ONE BILLION DOLLARS on Democrats While Your Grandkids Can’t Read at Grade Level

2026-05-01

Florida Strips Away All of Democrats Redistricting Wins in One Fell Swoop

2026-04-30

Ilhan Omar Read World War II as World War Eleven and Newsweek Rushes to Defend Her

2026-04-30

The DNC Paid for a Report Explaining Why They Lost — And Now They’re Too Scared to Let Anyone Read It

2026-04-29

She Works in Healthcare and Wished the Shooter Hadn’t Missed — Guess Who’s Filing for Unemployment

2026-04-29

Jimmy Kimmel Doubles Down on his Joke About Melania Being a Widow After WHCD Shooting–Are You Buying His Excuse?

2026-04-28

North Carolina Democrats Are Fleeing Their Own Party Like It’s on Fire — And the Chairwoman Just Told Them to Get Lost

2026-04-28

A Hollywood Actress Just Told Her Own Side to Shut Up After the WHCD Shooting — And the Left Is Melting Down Over It

2026-04-27

Jimmy Kimmel Joked About Trump Dying at the WHCD — Hours Later Someone Tried to Make It Happen at the Same Event

2026-04-27

Texas Said ‘No More DEI’ — University Staffers Said ‘Watch Me’ — Hidden Cameras Said ‘You’re Fired’

2026-04-26

Fetterman Just Told His Own Party to ‘Drop the TDS’ And Not a Single Democrat Knows What to Do With That

2026-04-26

The Pentagon Just Told Our NATO ‘Allies’ to Start Packing — And Spain Might Be First Out the Door

2026-04-24

A Trans-Identifying Father Allegedly Kidnapped His Own Child and Fled to CUBA for Surgery — So Trump’s FBI Went and Got the Kid Back

2026-04-24

A Liberal Polling Group Just Handed Trump the Best Argument for Ending Birthright Citizenship — And They Don’t Even Realize It

2026-04-24

Thirty Years of Data Just Proved Every Parent Who Questioned Child Gender Transitions Was Right — And the Medical Establishment Owes Them an Apology

2026-04-24

The Gates Foundation Just Fired 500 People and Ordered an Epstein Review — Which Means Whatever They Already Know Is Terrifying

2026-04-23

Senate Republicans Win! Take the First Step to Fully Fund ICE — And Democrats Stayed Up All Night Crying About It

2026-04-23

Vivek Ramaswamy Just Put $25 Million of His Own Money Into Ohio’s Governor’s Race — And His Democrat Opponent Should Be Nervous

2026-04-22

The ‘Anonymous Whistleblower’s’ Secret Helper Was a Russiagate Operative the Whole Time — And They’re STILL Working Together

2026-04-22

250 Journalists Just Signed a Letter Admitting They’re Activists — And They Want You to Watch Them Heckle the President at a Fancy Dinner

2026-04-21

The Washington Post’s Own Editor Just Admitted They Hid Biden’s Mental Decline from Voters

2026-04-21

The Biden Legacy in One Stat: One Out of Every Ten Babies Born Under Biden Was an Anchor Baby

2026-04-20

350,000 Dead People Are Still Registered to Vote — And Democrats Are Fighting in Court to Keep Them There

2026-04-20

Snopes Just Declared It UNETHICAL to Stop Giving Prisoners Free Hormone Treatments Because Apparently Jail Is a Spa Now

2026-04-19

George Soros Just Wrote a $50 Million Check to Buy the 2026 Midterms

2026-04-19

DoorDash Driver Tampers With Trump Supporter’s Food Then Cries on Camera When Real Life Shows Up

2026-04-17

Democrats Vote to Kill Impeachment Against One of Their Own Despite Saying Its Their Constitutional Duty to Hold Leaders Accountable

2026-04-17

The Networks That Broadcast Every Second of Impeachment Won’t Show You the Receipts Proving It Was a Sham

2026-04-17

Morning Joe Just Said the Quiet Part Out Loud About Trump and Iran — And Their Own Audience Can’t Believe It

2026-04-17

Woke College that Gave No-Grades or Majors and Charged $70,000 a Year Closes –The Market Spoke Louder Than Any Protest

2026-04-16

Mamdani’s ‘Free’ Grocery Store Will Cost $30 Million and Won’t Even Open Until 2029 — Socialism So Efficient You’ll Starve Waiting in Line

2026-04-16

New Social Security Increase Prediction

2026-04-14

America’s #1 Retirement Question Answered

2026-04-13

Retirement Just Got 15% More Difficult

2026-04-09

Fidelity, AARP Issue New Retirement Plan Warning

2026-04-08

The Retirement Number Everyone Trusts May Betray You

2026-04-06

The Average 401(k) Balance For Gen X

2026-04-02

We’re Entering A Social Security Disaster

2026-04-01

White House Clears New 401(k) Options

2026-03-31

Retirement Spending Survey – These Numbers Are Shocking!

2026-03-27

The Part-Time Job Trap (Social Security Penalty)

2026-03-26

The IRS Won’t Tell You About These Tax-Draining Blunders

2026-03-25

The Hidden Trap Waiting Inside Every Early Retirement Dream

2026-03-23

Where Are Retirees Moving To?

2026-03-19

New Financial Trend Sweeps America

2026-03-18

Could Social Security Be Cut By 24%?

2026-03-17

Social Security Announcement Shocks Nation

2026-03-17

The Worst 401(k) Mistake When Leaving A Job

2026-03-12

Vanguard Gives Shocking Retirement Account Notice

2026-03-09

The Retirement Rehearsal That Prevents Regret

2026-03-05

You’re Sitting on a Hidden Income Stream

2026-03-05

How to Handle the Retirement Pay Cut

2026-03-03

The Retirement Spending Shift That Boosts Happiness

2026-03-02

Don’t Let Taxes Hijack Your Legacy

2026-02-28

How To Organize Your Retirement Paycheck

2026-02-26

Can Your Retirement Survive a Shock?

2026-02-25

The Retirement Money Talk Most Couples Avoid

2026-02-23

The Retirement Spending Problem No One Talks About

2026-02-19

What Most Retirees Do Wrong With a Big Check

2026-02-18

The Two-Bucket Retirement Secret

2026-02-17

How to Keep Investing Without the Stress

2026-02-13

The Retirement Bridge Advantage

2026-02-12

The Roth Bracket-Fill Advantage

2026-02-11

Who Really Gets Your Retirement Money

2026-02-09

The February Tax Advantage

2026-02-05

5 Numbers to Check Yearly

2026-02-04

Why One Account Isn’t Enough

2026-02-03

Work in Retirement—Without Penalties

2026-01-30

The Right Order to Withdraw

2026-01-29

Spend Without Fear During Retirement

2026-01-28

The New Elder Fraud Epidemic

2026-01-26

The Best Way To Turn Your Home Into Income

2026-01-22

Homeownership Isn’t Always Freedom

2026-01-21

How Retirees Really Spend Money

2026-01-20

The $200,000 Retirement Blind Spot

2026-01-16

The IRS Loves It When You Make This Mistake

2026-01-15

Medicare 2026: How Rising Premiums Can Blindside Your Retirement Budget

2026-01-14

Pension Choices: Lump Sum or Monthly Annuity? The One Rule That Helps You Decide

2026-01-12

Use the 2026 Tax Brackets Like a Pro: How Retirees Can Shrink Lifetime Taxes

2026-01-08

Planning to Age 95: Smart—or Overkill?

2026-01-07

Why the First 5 Years of Retirement Are the Most Dangerous—and How to Protect Yourself

2026-01-06

The 62/70 Split Strategy That Can Boost Lifetime Income

2025-12-31